IOL Fluorochemical Weekly Report: Refrigerant Demand Recovers, Market Fluctuates at High Levels

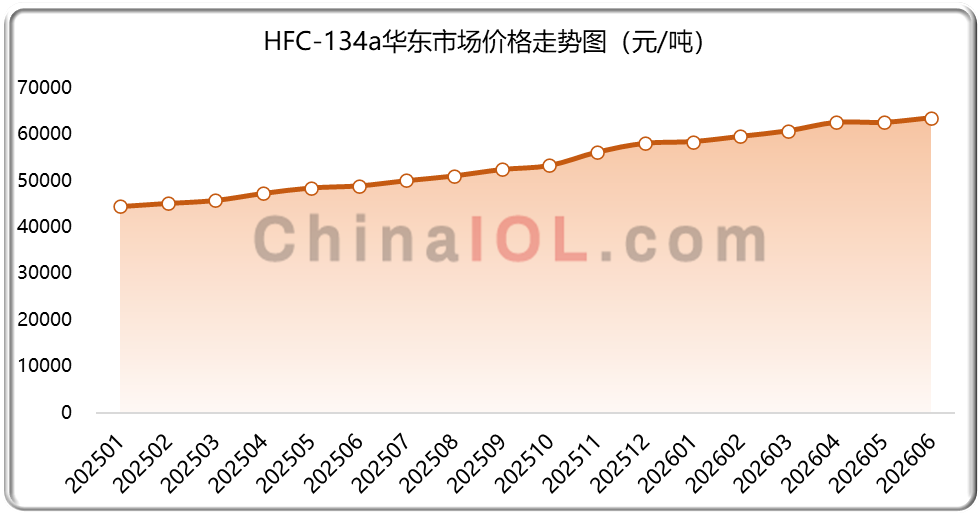

Refrigerant: Quota support and seasonal demand recovery drive price fluctuations and upward trends

This week, refrigerant demand rebounded, with the market fluctuating at elevated levels overall. Weekly market characteristics: Year-on-year production was constrained by rigid quotas, while mainstream refrigerant manufacturers operated normally, showing strong intent to maintain prices. However, due to sluggish exports in the foreign trade market, some factories reduced production capacity, leading to rising industry inventories. Upstream raw material prices declined more often than they rose under the dual pressures of high cost burdens and weak demand. Amid international conflicts, imported products such as sulfur, methanol, and petroleum faced widespread shortages and price surges. Overall demand steadily recovered, with notable structural divergence: domestic seasonal demand drove steady consumption, and end-user procurement progressed methodically. Meanwhile, geopolitical disruptions overseas temporarily impacted foreign trade flows. There was a mixed tone in policy adjustments. The U.S. and U.K. delayed the phase-out timeline for high-GWP refrigerants, benefiting overseas restocking demand for R134a and R410A. In contrast, the EU's refrigerant substitution policy was rigidly implemented, with a clear transition cycle for R32, and European pre-stocking efforts continued to support export demand. With dual supply-demand support in the short term, refrigerant prices are expected to remain at high levels and fluctuate.

ChinaIOL

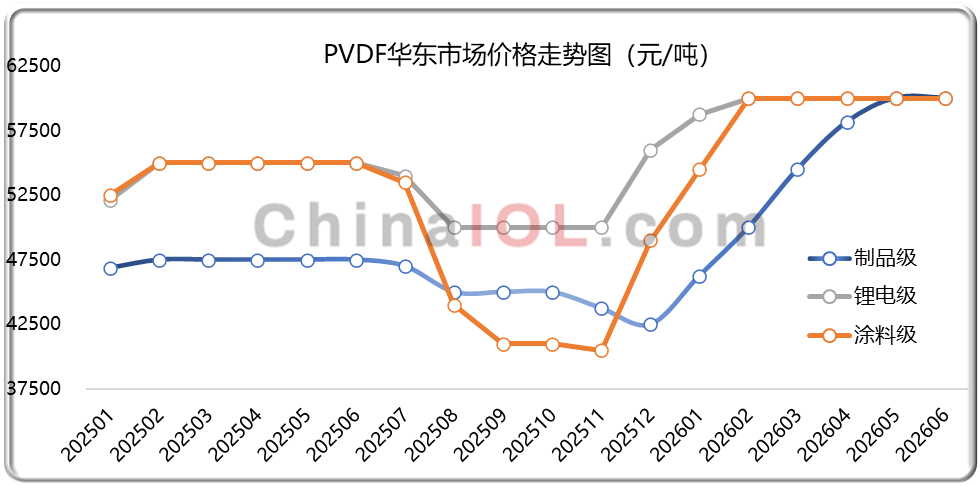

Fluorine-containing polymers: Cost support and factory price maintenance coexist, with upstream and downstream negotiations at a stalemate

This week, manufacturers in the fluoropolymer market generally maintained firm pricing, with upstream and downstream players locked in a stalemate, and mainstream products remaining stable. On the cost side, prices of upstream raw materials such as fluorite and hydrofluoric acid edged lower, but overall remained at elevated levels, providing strong cost support to downstream sectors. On the supply side, production facilities operated at high capacity, increasing supply and leading to a gradual rise in supply-demand pressure. On the demand side, downstream inventory from earlier stockpiling remained to be cleared, resulting in cautious purchasing activity. The market exhibited structural divergence: demand for premium categories remained resilient, with incremental shipments and stable quotations, while mid-to-low-end products faced sluggish demand, flat transactions, and weaker prices. Affected by structural supply-demand imbalances, product performance across grades continued to diverge. In summary, supported by raw material costs and manufacturers' pricing intentions, the market is expected to maintain a stalemate and consolidation trend in the short term.

Weekly Highlights

01The U.S. has issued its final ruling on the first sunset review of anti-dumping duties on Chinese R32

On May 28, the U.S. Department of Commerce issued an official ruling notice in the Federal Register, concluding the first round of expedited sunset review for anti-dumping duties on R32 refrigerant (difluoromethane) originating from China. The key ruling conclusions were clarified, maintaining trade barriers against Chinese R32 imports. In this first-round expedited sunset review, the U.S. ultimately determined that lifting the current anti-dumping measures would result in the continued or renewed dumping of Chinese products at a rate of 221.06%.

02Jinshi Resources Zhejiang Mine Participates in Special Inspection Involving Approximately 30,000 Tons of Monthly Capacity

On the evening of May 31, Jinshi Resources (603505) announced that to comply with the special inspection and review of underground mines conducted by the emergency management department of Zhejiang Province, several of its fluorite mines in Zhejiang have entered a phased shutdown, rectification, or pending review status. The affected mines account for approximately 30,000 tons of monthly production capacity, which is expected to impact the company's fluorite production plan for 2026 and short-term operational performance. In response to the phased shutdown of mines in Zhejiang, Jinshi Resources has formulated a contingency plan, including intensifying the sales of existing fluorite inventory and coordinating production and sales arrangements for subsidiaries outside the province to mitigate the impact of production capacity fluctuations.

03Juhua Shares: PTFE production capacity of 28,000 tons/year, with another 37,000 tons/year under construction

Recently, Juhua Co., Ltd. responded to investor inquiries on the interactive platform, stating that the company has completed the construction and put into operation a 10,000-ton/year production line for high-quality meltable fluororesin (PFA). After testing and verification by semiconductor clients, the product's metal ion content meets the SEMI F57 standard requirements, making it suitable for semiconductor wet processes, chemical storage and transportation, and key components of high-end equipment, serving as an alternative to imported products. By the end of 2025, the company will have a PTFE production capacity of 28,000 tons/year, with an additional 37,000 tons/year under construction. Currently, the company is actively advancing cooperation with clients in the electronics and semiconductor sectors. The Gansu Juhua construction project is scheduled for handover on June 30, 2026, after which the company will steadily proceed with single-unit testing, integrated testing, and chemical feed trial operations.

04Announcement of the PVDF Polymerization Technology Upgrading Project at Shandong Huian

On May 29, the Zibo Municipal Ecological Environment Bureau announced the acceptance of the Environmental Impact Assessment Report for the PVDF Polymerization Technology Upgrade Project of Shandong Hua'an New Materials Co., Ltd. The project plans to invest 15 million yuan and will increase PVDF production by 8,000 tons/year (based on finished PVDF output) upon completion. The total annual PVDF production capacity of the plant will reach 22,000 tons/year, with the first and second-phase polymerization workshops contributing 10,000 tons/year and the third-phase polymerization workshop contributing 12,000 tons/year. The construction period for the project is 6 months.